If you’re a business operator looking for ways to optimize cash flow and boost your company’s financial health, leveraging the 2/10 net 30 payment terms is a smart strategy. Here’s how you can use this technique to secure free financing for your business.

What is 2/10 Net 30?

The 2/10 net 30 payment terms mean that if you pay your invoice within 10 days, you receive a 2% discount. If you don’t take the discount, the full payment is due in 30 days. This can be a great way to save money, but many businesses overlook the potential for using this term strategically to get free financing.

Understanding 2/10 Net 30

2: The discount applied to an early payment

10: The number of days after an invoice has been issued. For example, if an order is delivered on Jan 1st, the 10 days would refer to payment made on or before Jan 11th.

Net 30: The terms provided without a discount. For example, the same order delivered on Jan 1st would be due by Jan 31st at par value.

Note: This is a simple naming convention, but the prices may change. Your vendors may charge a larger discount (say, 3%) for earlier payment or offer a full price beyond 30 days (say, net 45).

Why Do Vendors Offer Discounts

Vendors offer 2/10 net 30 discounts to accelerate their cash flow and reduce the risk of non-payment. By incentivizing early payment, they can receive funds more quickly, which helps in managing their cash more effectively, reducing the need for external financing, and lowering financing costs. Additionally, offering such discounts can strengthen customer relationships, create a competitive advantage, and reduce administrative costs associated with managing accounts receivable. This strategy helps vendors maintain a steady flow of funds, optimize inventory management, and improve overall financial stability.

Step-by-Step Guide to Get Free Financing Using 2/10 Net 30

Using 2/10 net 30 terms with a reverse factoring company allows businesses to secure 10 days of free financing. By negotiating these terms with your vendor, partnering with a reverse factoring company to pay the invoice on the 10th day, and then repaying the factoring company within 30 days, you save the 2% early payment discount while paying the reverse factoring company, typically, 2% or less.

In fact, according to a recent McKinsey & Company report, reverse factoring is one of the fastest growing forms of financing. This strategy boosts your cash balance, enhances liquidity, and creates opportunities for growth, ultimately increasing your business’s enterprise value.

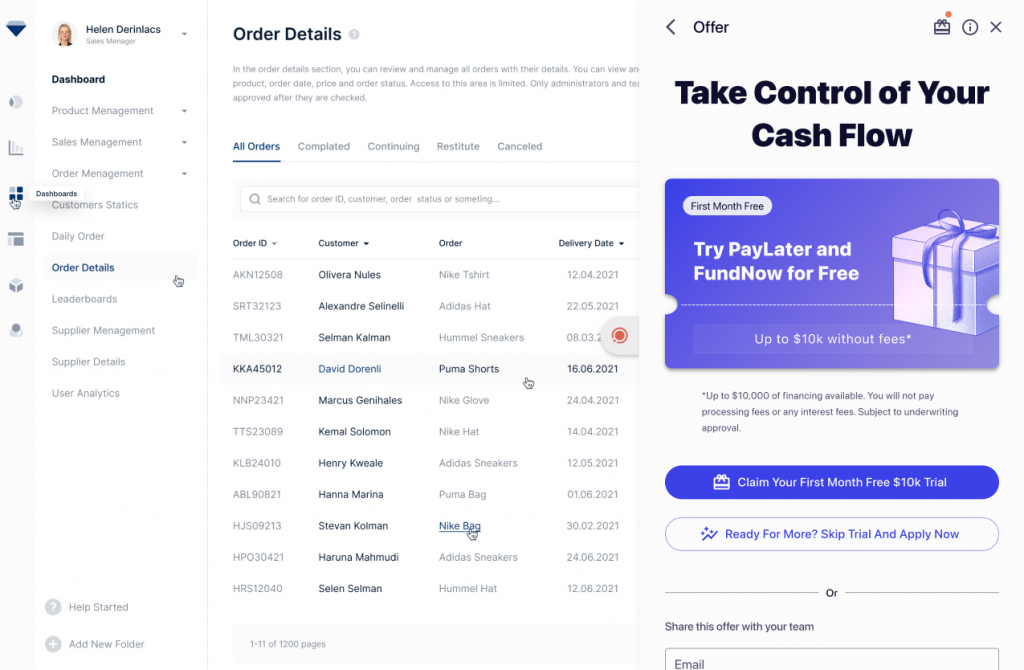

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

How to Get Started

1. Negotiate 2/10 Net 30 Terms with Your Vendor:

Discuss the early payment options with your vendor and encourage them to offer 2/10 net 30 terms. This is the foundation of the strategy.

Hint: Your vendor may not immediately offer 2/10 net 30, but they will often take a discount for early payment. Start the conversation by asking your vendor if they take an early pay discount – they may be more open than you think!

2. Work with a Reverse Factoring Company:

Partner with a reverse factoring company that will pay your invoice on the 10th day. By doing this, you take advantage of the 2% discount offered by the vendor.

Reverse factoring companies may charge less than the 2% discount offered to your vendor. Before committing to terms, work with your reverse factoring partner to see if you can pay under 2%.

3. Instruct the Reverse Factoring Company to Pay Your Vendor on Day 10.

This process may be manual, but where possible work with a reverse factoring company that utilizes technology to facilitate the process. This is typically in the form of an invoice portal that can help manage your payments and reporting.

Make sure to maintain good communication with your vendor and reverse factoring company. This strategy is dependent on your vendor receiving timely payment and accepting the discount.

4. Pay Back the Reverse Factoring Company on Day 40:

Once the invoice has been paid, you will typically have 30 days to pay back the reverse factoring company. Typically, the fees charged by the reverse factoring company for this service will be around 2%, but may be less.

Hint: It may be worth exploring long payypment options with your reverse factoring company. Many financiers will extend your due date from 30 days to 60 or 90 days for an additional fee, often called a factor rate. Depending on the offer, this may be a good option to pull out cash from your working capital cycle.

Fees charged by the reverse factoring company… will be around 2%, but may be less.

Make sure to negotiate with the lender to drive lowest price.

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

Benefits of Reverse Factoring on 2/10 Net 30

1. Free Financing for 10 Days:

By using the reverse factoring company, you effectively get 10 days of free financing. You save the 2% discount and then pay it as a fee to the reverse factoring company without any additional cost.

2. Boost Cash Balance:

This strategy helps you maintain a healthier cash balance, providing more liquidity for day-to-day operations or unexpected expenses.

3. Increase Growth Opportunities:

With improved cash flow, you have more opportunities to invest in growth projects, whether it’s expanding your product line, investing in marketing, or improving infrastructure.

4. Grow Enterprise Value:

Enhanced cash flow and better financial management can lead to an increase in your business’s enterprise value, making it more attractive to investors and stakeholders.

Why Every Business Should Use Reverse Factoring on 2/10 Net 30

This simple yet effective technique allows you to optimize your payment terms, improve cash flow, and get free financing without taking on additional risk. It’s a strategy that every business operator should consider to enhance their financial health and drive growth.

By strategically using 2/10 net 30 terms and partnering with a reverse factoring company, you can turn a standard vendor payment term into a powerful financial tool. Start implementing this technique today and see the positive impact it can have on your business’s financial stability and growth potential.

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.