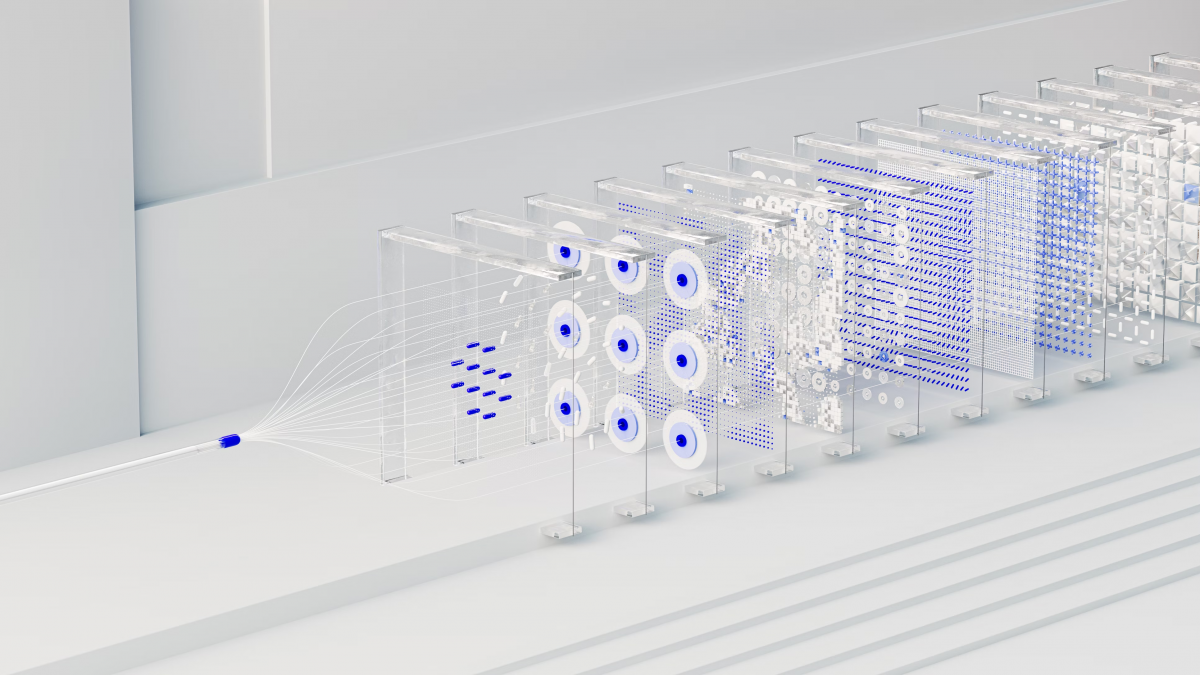

Traditional credit policies rely heavily on surface-level / summary data like credit scores and historical financial statements, which often fail to capture the full picture of a business’s financial health. As a result, many small-medium enterprises (SMEs) are either mis-evaluated, leading to higher rejection rates, or inflated interest rates, or unnecessary risk exposure. The shortcomings of these policies result in missed opportunities for both lenders and borrowers, as they fail to account for the dynamic nature of business operations.

Recognizing these limitations, we built a new credit policy leveraging AI and real-time data integration. Our solution taps into granular financial and operational data from business management systems like ERP, point of sale (POS), accounting, and supply chain platforms. By analyzing trends and qualities such as customer concentration, payment patterns, sales consistency and owner integrity, our AI models provide a more nuanced assessment of a company’s risk. This approach enables lenders to offer more accurate, tailored loan products, reducing the likelihood of defaults and improving access to capital for creditworthy SMEs.

The impact of this new policy is profound. By moving beyond traditional, heuristic-based methods, lenders can make data-driven decisions that reflect the true risk profile of a business, in minutes. This leads to lower default rates, more competitive loan terms, a broader pool of eligible borrowers, and dynamic optimizations. Ultimately, a modern credit policy benefits both SMEs and lenders, fostering sustainable growth and driving innovation in the lending landscape.

fde9a119-ae18-48b1-a429-8688f95338bc

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

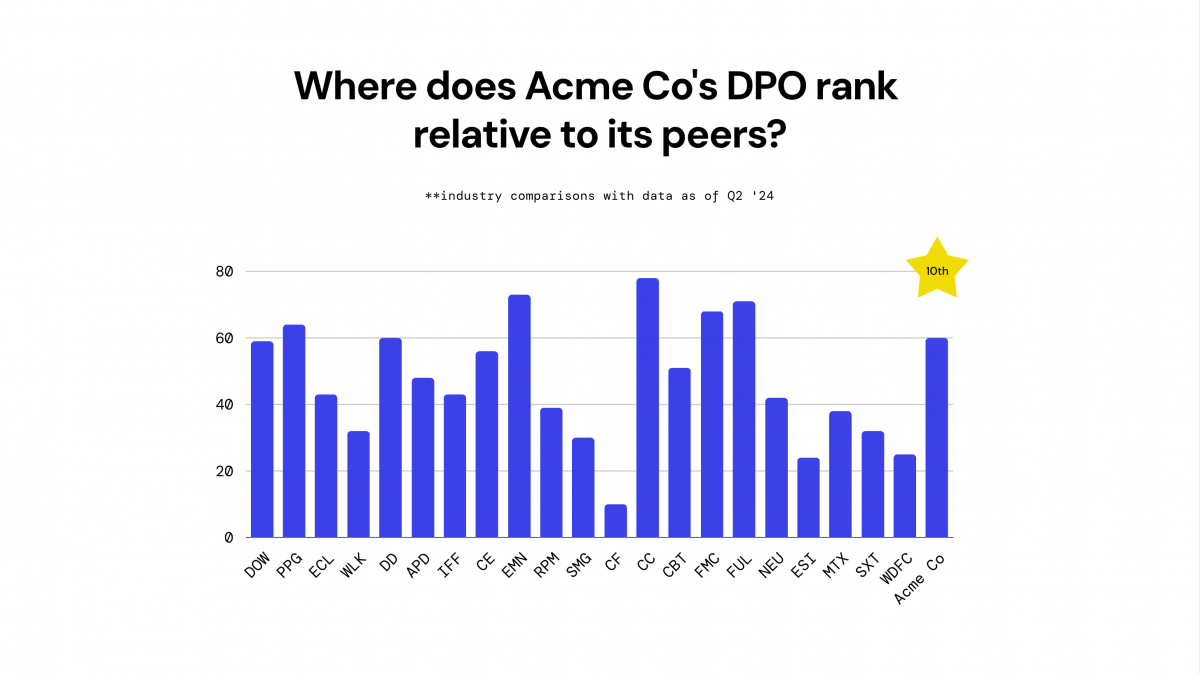

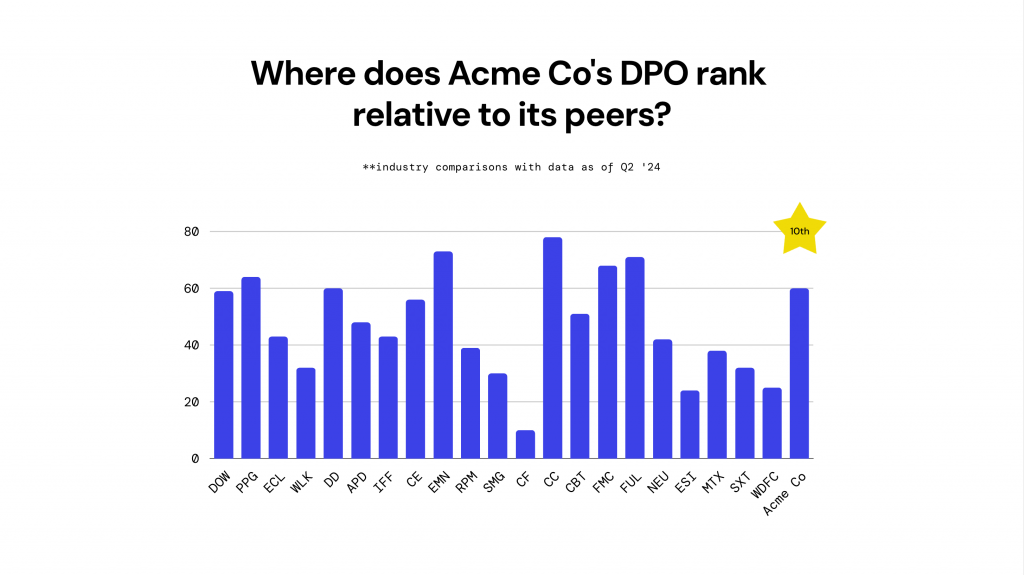

Managing your cash conversion cycle (CCC) is vital for optimizing your working capital and maintaining the financial health of your business. The CCC measures the time it takes for a company to convert its investments in inventory and other resources into cash flows from sales. Effective management of this cycle helps reduce financing costs, improve liquidity, and increase profitability. Most companies have a CCC greater than 30 days, meaning their cash is tied up for extended periods. By actively managing your working capital, you can shorten your CCC, freeing up cash to reinvest in your operations and fuel growth.

The CCC is a key barometer of how efficiently you manage your business. A shorter cycle indicates effective inventory management, prompt collection of receivables, and strategic handling of payables—all signs of a well-run company. Benchmarking your CCC against industry peers provides valuable insights into your operational efficiency and areas for improvement. We invite you to download our free working capital analysis to access a benchmarking tool that compares your CCC with that of your peers, helping you identify opportunities to optimize your working capital management.

In today’s fast-paced digital landscape, businesses are seeking more than just software solutions from their vertical SaaS and ERP providers—they’re looking for complete tools that help them grow and navigate financial challenges. For many companies, especially small and medium-sized enterprises (SMEs), access to working capital is a critical need, often determining whether they can expand, improve operations, or even maintain day-to-day functions.

To meet this growing demand, vertical SaaS and ERP platforms are beginning to embed lending solutions directly into their software. This integration provides businesses with the financial tools they need while keeping them within the platforms they already rely on. By embedding lending, software providers not only add significant value for their users but also open new revenue streams and strengthen customer loyalty.

What is Embedded Lending?

Embedded lending refers to the seamless integration of lending services directly into a platform or application, allowing businesses to offer financing options at the point of need. Rather than requiring users to seek external loans or credit, embedded lending provides access to financing within the same platform they already use for their operations, such as an ERP system or e-commerce platform. This simplifies the borrowing process, speeds up approval times, and creates a more convenient experience for users. It even lowers rates!

For example, a vertical SaaS company focused on online retail might offer embedded lending by allowing customers to finance their purchases with a buy-now-pay-later option integrated into the checkout process. A business customer purchasing $10,000 worth of products can choose to finance the transaction with flexible payment terms.

The embedded lending system instantly evaluates the customer’s creditworthiness and approves the loan within seconds, all without disrupting the shopping experience. This integration not only improves conversion rates by making purchases more affordable but also creates a streamlined, seamless process for both the wholesale retailer and its customer.

Why Your Customers May Need Embedded Lending Solutions

For SMEs, accessing capital can be a major hurdle. Traditional lending processes are often slow, cumbersome, and difficult to navigate, with many businesses struggling to secure the funding they need in time to address pressing concerns. As a result, companies may face cash flow shortages, limiting their ability to grow, invest in new projects, or even meet immediate operational needs.

This is where vertical SaaS and ERP platforms have a unique opportunity. By embedding lending services directly into their software, they offer users a simple, streamlined way to access working capital without leaving the platform. With this integration, users can secure financing quickly and efficiently, enabling them to focus on running their business.

Embedded lending offers a new promise for more affordable credit solutions.

How Embedded Lending Adds Value

When vertical SaaS and ERP platforms offer embedded lending, they provide users with a seamless financial solution that’s fully integrated with their operational tools. Here’s how this benefits both the software provider and the end-user:

Solving Cash Flow Challenges: By offering tailored lending options, platforms can help users bridge cash flow gaps, fund new projects, or purchase critical materials without needing to apply through traditional banks.

Enhanced User Experience: Embedded lending keeps users within the software environment they’re familiar with, reducing the friction of dealing with external lenders and manual application processes.

Increased Customer Retention: When businesses know they can rely on their SaaS or ERP platform for both operational management and financial support, their loyalty increases, reducing churn and improving lifetime customer value.

According to a recent McKinsey & Company report, embedded lending is growing along with the embedded finance market at 15-20% y/y.

By 2030, the embedded lending market could surpass $100 billion and account for 10 to 15 percent of banking revenue pools.

McKinsey & Company

Key Advantages to Embedded Lending

One of the key advantages of embedding lending into vertical SaaS and ERP platforms is the ability to offer financial solutions that are tailored to specific industries. SaaS platforms that cater to niche markets—whether it’s construction, healthcare, retail, or another field—have deep insights into their users’ operations and financial needs. This allows them to offer more personalized lending options than traditional financial institutions.

For instance, a SaaS platform designed for construction businesses could offer financing solutions aimed at helping companies purchase materials or cover payroll between project payments. Similarly, an ERP system for chemical businesses might provide short-term loans to help manage seasonal inventory or fluctuating demand.

Datacor, an ERP company focused on process manufacturers and distributors, partners with Lendica to offer its customers A/R and A/P loans embedded into their invoicing tools. This service allows businesses to access working capital by borrowing against future invoices, streamlining the process with a few clicks, helping businesses manage cash flow and expand more easily.

1. Drive New Revenue Streams

For SaaS and ERP providers, embedding lending is more than just adding value for users—it’s a way to unlock new revenue streams. By partnering with financial institutions, these platforms can earn referral fees, commissions, or revenue shares on lending transactions facilitated through their software.

This additional revenue can be reinvested into the platform, driving further innovation and expanding service offerings. As more users take advantage of embedded lending, the platform’s profitability increases without needing to introduce significant changes to its core product.

2. Strengthen Your Competitive Edge

In an increasingly crowded SaaS and ERP market, platforms must find ways to differentiate themselves. Embedding lending solutions is a powerful way to stand out from competitors by offering an all-in-one solution that meets both operational and financial needs.

As industries continue to shift towards digital-first solutions, platforms that offer embedded lending will be seen as leaders in innovation. By providing comprehensive tools that help users manage all aspects of their business—from operations to financing—SaaS and ERP platforms can solidify their place as essential partners in their customers’ success.

3. Future Proof Your Vertical SaaS and ERP Platform

The integration of lending solutions into vertical SaaS and ERP platforms is a natural evolution in the digital economy. By offering embedded lending, these platforms can solve one of the most pressing challenges their users face: access to capital. This not only adds significant value for users but also creates new revenue opportunities and strengthens customer loyalty.

As industries become more reliant on digital solutions to manage both operations and finances, SaaS and ERP platforms that embrace embedded lending will position themselves as leaders in their space, helping their customers thrive in an ever-changing business landscape.

Lendica has helped thousands of small and medium-sized enterprises (SMEs) with efficient, non-dilutive capital during critical growth periods. As word spreads, we often find ourselves alongside traditional banks in client meetings. Despite access to prime rates from banks, clients still ask: Why should I use Lendica?

In this post, we will share several use cases that our clients have flagged as key benefits to using Lendica’s fast, affordable capital tools instead of relying on traditional banking relationships.

1. Freeing Your Team from Tedious Paperwork

How many hours does your finance team spend communicating with banks? This goes beyond the initial credit approval process and continues throughout the year:

• Providing constant updates on “proof of business” documents

• Submitting buyer and supplier contact lists for background checks

• Preparing cargo receipts and invoices for loan drawdowns

This manual, time-consuming process is central to how banks assess your business. Even after months of paperwork and approval, the burden doesn’t end—each new funding checkpoint brings these processes back.

Lendica changes the game by using technology to gather and analyze data that would take banks months to process. By integrating with your ERP system, our software automatically assesses your financial health, allowing lending decisions in minutes instead of months. Your finance team can now focus on business development and contract negotiations rather than endless paperwork.

Plus, your employees won’t need to learn new systems—everything is managed within your existing ERP, with every invoice seamlessly linked to funding.

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

Think a prime rate from the bank is the only cost you’re paying? Consider these hidden fees:

• Handling commissions, small bill charges, commitment fees, service charges, annual review fees, third-party vendor fees, foreign exchange fees, and more.

Additionally, have you accounted for indirect costs like:

• Holding security deposits

• Purchasing bundled investment or insurance products

• Committing to move certain funds through the bank

At Lendica, AI handles the heavy lifting, so we don’t need an extensive back-office team, and we don’t attach unnecessary strings. That’s why our pricing is straightforward and fair. Our AI also learns about your business over time, ensuring your pricing reflects the true nature of your operations.

3. Flexible Terms with Fewer Restrictions

Banks operate with limited flexibility and often require various guarantees and covenants, such as:

• Personal or corporate guarantees

• Pledging real estate assets

• Notifying trade partners about borrowing arrangements

• Restrictions on repayment dates

• Prohibitions on early repayment

• Monthly onsite audits and strict financial ratio adherence

Lendica provides customized solutions with far greater flexibility. We can tailor the loan amount, repayment schedule, and interest rates to meet your unique needs. And because we operate in real-time with your business, we understand your financial health without needing collateral like real estate or personal assets. Just use the capital as part of your business, no strings attached.

The Lendica Advantage

For SMEs seeking fast, flexible, and accessible credit, Lendica offers clear advantages over traditional banks. With superior data analysis, transparent pricing, flexible terms, and unmatched convenience, we’re transforming the way businesses access capital. Ready to experience the difference? Let’s get plugged in!

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.