Traditional credit policies rely heavily on surface-level / summary data like credit scores and historical financial statements, which often fail to capture the full picture of a business’s financial health. As a result, many small-medium enterprises (SMEs) are either mis-evaluated, leading to higher rejection rates, or inflated interest rates, or unnecessary risk exposure. The shortcomings of these policies result in missed opportunities for both lenders and borrowers, as they fail to account for the dynamic nature of business operations.

Recognizing these limitations, we built a new credit policy leveraging AI and real-time data integration. Our solution taps into granular financial and operational data from business management systems like ERP, point of sale (POS), accounting, and supply chain platforms. By analyzing trends and qualities such as customer concentration, payment patterns, sales consistency and owner integrity, our AI models provide a more nuanced assessment of a company’s risk. This approach enables lenders to offer more accurate, tailored loan products, reducing the likelihood of defaults and improving access to capital for creditworthy SMEs.

The impact of this new policy is profound. By moving beyond traditional, heuristic-based methods, lenders can make data-driven decisions that reflect the true risk profile of a business, in minutes. This leads to lower default rates, more competitive loan terms, a broader pool of eligible borrowers, and dynamic optimizations. Ultimately, a modern credit policy benefits both SMEs and lenders, fostering sustainable growth and driving innovation in the lending landscape.

fde9a119-ae18-48b1-a429-8688f95338bc

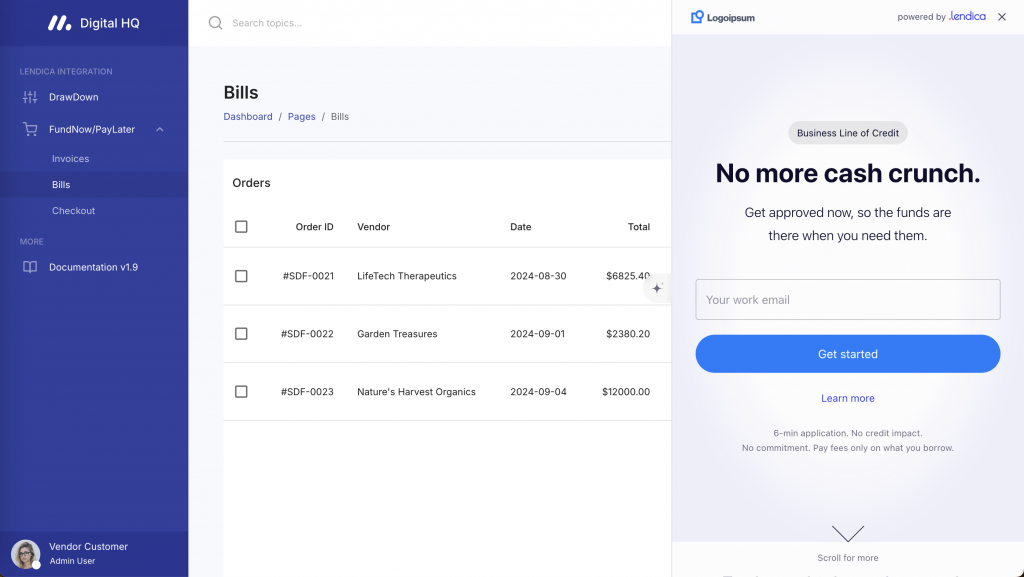

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

In today’s fast-paced digital landscape, businesses are seeking more than just software solutions from their vertical SaaS and ERP providers—they’re looking for complete tools that help them grow and navigate financial challenges. For many companies, especially small and medium-sized enterprises (SMEs), access to working capital is a critical need, often determining whether they can expand, improve operations, or even maintain day-to-day functions.

To meet this growing demand, vertical SaaS and ERP platforms are beginning to embed lending solutions directly into their software. This integration provides businesses with the financial tools they need while keeping them within the platforms they already rely on. By embedding lending, software providers not only add significant value for their users but also open new revenue streams and strengthen customer loyalty.

What is Embedded Lending?

Embedded lending refers to the seamless integration of lending services directly into a platform or application, allowing businesses to offer financing options at the point of need. Rather than requiring users to seek external loans or credit, embedded lending provides access to financing within the same platform they already use for their operations, such as an ERP system or e-commerce platform. This simplifies the borrowing process, speeds up approval times, and creates a more convenient experience for users. It even lowers rates!

For example, a vertical SaaS company focused on online retail might offer embedded lending by allowing customers to finance their purchases with a buy-now-pay-later option integrated into the checkout process. A business customer purchasing $10,000 worth of products can choose to finance the transaction with flexible payment terms.

The embedded lending system instantly evaluates the customer’s creditworthiness and approves the loan within seconds, all without disrupting the shopping experience. This integration not only improves conversion rates by making purchases more affordable but also creates a streamlined, seamless process for both the wholesale retailer and its customer.

Why Your Customers May Need Embedded Lending Solutions

For SMEs, accessing capital can be a major hurdle. Traditional lending processes are often slow, cumbersome, and difficult to navigate, with many businesses struggling to secure the funding they need in time to address pressing concerns. As a result, companies may face cash flow shortages, limiting their ability to grow, invest in new projects, or even meet immediate operational needs.

This is where vertical SaaS and ERP platforms have a unique opportunity. By embedding lending services directly into their software, they offer users a simple, streamlined way to access working capital without leaving the platform. With this integration, users can secure financing quickly and efficiently, enabling them to focus on running their business.

Embedded lending offers a new promise for more affordable credit solutions.

How Embedded Lending Adds Value

When vertical SaaS and ERP platforms offer embedded lending, they provide users with a seamless financial solution that’s fully integrated with their operational tools. Here’s how this benefits both the software provider and the end-user:

Solving Cash Flow Challenges: By offering tailored lending options, platforms can help users bridge cash flow gaps, fund new projects, or purchase critical materials without needing to apply through traditional banks.

Enhanced User Experience: Embedded lending keeps users within the software environment they’re familiar with, reducing the friction of dealing with external lenders and manual application processes.

Increased Customer Retention: When businesses know they can rely on their SaaS or ERP platform for both operational management and financial support, their loyalty increases, reducing churn and improving lifetime customer value.

According to a recent McKinsey & Company report, embedded lending is growing along with the embedded finance market at 15-20% y/y.

By 2030, the embedded lending market could surpass $100 billion and account for 10 to 15 percent of banking revenue pools.

McKinsey & Company

Key Advantages to Embedded Lending

One of the key advantages of embedding lending into vertical SaaS and ERP platforms is the ability to offer financial solutions that are tailored to specific industries. SaaS platforms that cater to niche markets—whether it’s construction, healthcare, retail, or another field—have deep insights into their users’ operations and financial needs. This allows them to offer more personalized lending options than traditional financial institutions.

For instance, a SaaS platform designed for construction businesses could offer financing solutions aimed at helping companies purchase materials or cover payroll between project payments. Similarly, an ERP system for chemical businesses might provide short-term loans to help manage seasonal inventory or fluctuating demand.

Datacor, an ERP company focused on process manufacturers and distributors, partners with Lendica to offer its customers A/R and A/P loans embedded into their invoicing tools. This service allows businesses to access working capital by borrowing against future invoices, streamlining the process with a few clicks, helping businesses manage cash flow and expand more easily.

1. Drive New Revenue Streams

For SaaS and ERP providers, embedding lending is more than just adding value for users—it’s a way to unlock new revenue streams. By partnering with financial institutions, these platforms can earn referral fees, commissions, or revenue shares on lending transactions facilitated through their software.

This additional revenue can be reinvested into the platform, driving further innovation and expanding service offerings. As more users take advantage of embedded lending, the platform’s profitability increases without needing to introduce significant changes to its core product.

2. Strengthen Your Competitive Edge

In an increasingly crowded SaaS and ERP market, platforms must find ways to differentiate themselves. Embedding lending solutions is a powerful way to stand out from competitors by offering an all-in-one solution that meets both operational and financial needs.

As industries continue to shift towards digital-first solutions, platforms that offer embedded lending will be seen as leaders in innovation. By providing comprehensive tools that help users manage all aspects of their business—from operations to financing—SaaS and ERP platforms can solidify their place as essential partners in their customers’ success.

3. Future Proof Your Vertical SaaS and ERP Platform

The integration of lending solutions into vertical SaaS and ERP platforms is a natural evolution in the digital economy. By offering embedded lending, these platforms can solve one of the most pressing challenges their users face: access to capital. This not only adds significant value for users but also creates new revenue opportunities and strengthens customer loyalty.

As industries become more reliant on digital solutions to manage both operations and finances, SaaS and ERP platforms that embrace embedded lending will position themselves as leaders in their space, helping their customers thrive in an ever-changing business landscape.

Lendica has helped thousands of small and medium-sized enterprises (SMEs) with efficient, non-dilutive capital during critical growth periods. As word spreads, we often find ourselves alongside traditional banks in client meetings. Despite access to prime rates from banks, clients still ask: Why should I use Lendica?

In this post, we will share several use cases that our clients have flagged as key benefits to using Lendica’s fast, affordable capital tools instead of relying on traditional banking relationships.

1. Freeing Your Team from Tedious Paperwork

How many hours does your finance team spend communicating with banks? This goes beyond the initial credit approval process and continues throughout the year:

• Providing constant updates on “proof of business” documents

• Submitting buyer and supplier contact lists for background checks

• Preparing cargo receipts and invoices for loan drawdowns

This manual, time-consuming process is central to how banks assess your business. Even after months of paperwork and approval, the burden doesn’t end—each new funding checkpoint brings these processes back.

Lendica changes the game by using technology to gather and analyze data that would take banks months to process. By integrating with your ERP system, our software automatically assesses your financial health, allowing lending decisions in minutes instead of months. Your finance team can now focus on business development and contract negotiations rather than endless paperwork.

Plus, your employees won’t need to learn new systems—everything is managed within your existing ERP, with every invoice seamlessly linked to funding.

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

Think a prime rate from the bank is the only cost you’re paying? Consider these hidden fees:

• Handling commissions, small bill charges, commitment fees, service charges, annual review fees, third-party vendor fees, foreign exchange fees, and more.

Additionally, have you accounted for indirect costs like:

• Holding security deposits

• Purchasing bundled investment or insurance products

• Committing to move certain funds through the bank

At Lendica, AI handles the heavy lifting, so we don’t need an extensive back-office team, and we don’t attach unnecessary strings. That’s why our pricing is straightforward and fair. Our AI also learns about your business over time, ensuring your pricing reflects the true nature of your operations.

3. Flexible Terms with Fewer Restrictions

Banks operate with limited flexibility and often require various guarantees and covenants, such as:

• Personal or corporate guarantees

• Pledging real estate assets

• Notifying trade partners about borrowing arrangements

• Restrictions on repayment dates

• Prohibitions on early repayment

• Monthly onsite audits and strict financial ratio adherence

Lendica provides customized solutions with far greater flexibility. We can tailor the loan amount, repayment schedule, and interest rates to meet your unique needs. And because we operate in real-time with your business, we understand your financial health without needing collateral like real estate or personal assets. Just use the capital as part of your business, no strings attached.

The Lendica Advantage

For SMEs seeking fast, flexible, and accessible credit, Lendica offers clear advantages over traditional banks. With superior data analysis, transparent pricing, flexible terms, and unmatched convenience, we’re transforming the way businesses access capital. Ready to experience the difference? Let’s get plugged in!

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

The solar industry is experiencing unprecedented growth, driven by the global shift towards renewable energy. However, with this rapid expansion comes significant financial challenges, particularly in managing cash flow and financing new projects. It’s reported that a substantial number of solar companies struggle or even fail due to insufficient funding, highlighting the critical importance of effective financial management. To navigate these challenges, many solar companies are turning to innovative financial strategies like factoring and reverse factoring, which are proving to be game-changers for the industry.

The Financial Challenges in the Solar Industry

Solar companies, like many in the construction and energy sectors, often face substantial upfront costs. These include purchasing materials, paying for labor, and covering other operational expenses. Compounding these challenges is the fact that payment for completed projects can be delayed for weeks or even months, while suppliers often demand payment upfront or on tight terms. This combination of factors can create severe cash flow issues, leading to project delays, missed opportunities, and in some cases, business failure.

Accounts Receivable: Factoring for Immediate Access to Capital

One of the most pressing challenges solar companies face is the delay in receiving payment after a project is completed. On average, it can take anywhere from 30 to 90 days to receive payment from clients after a project is finished. This delay can create a cash flow bottleneck, limiting the company’s ability to move forward with new projects. Factoring addresses this challenge by providing immediate access to funds the very same day a project is completed.

Through factoring, solar companies can sell their accounts receivable (invoices) to a third-party financial institution, often referred to as a factor. The factor advances a significant percentage of the invoice value—typically around 80-90%—to the company immediately, with the balance (minus a fee) paid once the client settles the invoice. This same-day funding capability allows companies to maintain cash flow and continue operations without interruption.

The benefits of factoring include:

Accelerated Cash Flow: Access to funds on the day of project completion ensures that solar companies can immediately reinvest in their next project or cover ongoing operational costs.

Reduced Financial Stress: Knowing that funds will be available the same day a project is completed eliminates the uncertainty and stress associated with delayed payments.

Enhanced Operational Efficiency: With immediate funding, companies can streamline their operations, reducing downtime between projects and increasing overall productivity.

Speed up cash collection with FundNow

Learn how you can get paid upfront on your sales invoices.

The solar industry is an integral part of world’s future energy consumption, but there are many challenges running a solar business.

Accounts Payable: Reverse Factoring to Extend Payment Terms

In addition to managing cash flow after project completion, solar companies also face significant upfront costs, particularly when purchasing the materials needed for installations. It’s estimated that up to 40-60% of a solar company’s capital can be tied up in purchasing materials for ongoing projects. Suppliers often require payment on tight terms, adding to the financial pressure. This is where reverse factoring, also known as supply chain financing, comes into play.

It is estimated that 40-60% of a solar company’s capital can be tied up in purchasing materials for ongoing projects.

IEA 50 Report

Reverse factoring allows solar companies to extend their payment terms with suppliers while ensuring that the suppliers are paid promptly. In this arrangement, a third-party financial institution pays the supplier on behalf of the solar company, and the company then repays the financial institution at a later date. This extension of payment terms gives solar companies the flexibility to manage their cash flow more effectively.

The advantages of reverse factoring include:

Extended Payment Terms: Solar companies can negotiate longer payment terms with their suppliers, reducing the immediate strain on their cash flow.

Improved Supplier Relationships: Suppliers receive prompt payment, which can strengthen relationships and potentially lead to better pricing or terms in the future.

Better Cash Flow Management: By aligning payment schedules with revenue cycles, solar companies can avoid the cash flow crunches that often accompany rapid growth or multiple simultaneous projects.

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

Integrated Financial Solutions in Solar SaaS Platforms

As the solar industry continues to embrace these financial strategies, many of the leading solar vertical SaaS platforms have begun integrating factoring and reverse factoring solutions into their systems. This integration makes it easier for solar companies to access these financial tools directly through the platforms they already use to manage their operations, streamlining the process and enhancing efficiency.

The Combined Power of Factoring and Reverse Factoring

When used together, factoring and reverse factoring create a powerful financial toolkit for solar companies. Factoring ensures that companies have immediate access to capital upon project completion, while reverse factoring provides the flexibility needed to manage material costs by extending payment terms. This combination allows solar companies to operate with greater financial stability, take on more projects, and ultimately grow their business more rapidly.

A Brighter Future for Solar Companies

As the solar industry continues to expand, the financial demands on companies within the sector will only increase. Factoring and reverse factoring solutions are tailored to meet these challenges, providing the tools solar companies need to thrive in a competitive marketplace. By offering same-day funding for completed projects, flexible financing options for material purchases, and a seamless application process, these financial strategies are empowering solar companies to accelerate their growth, improve their financial health, and contribute to the global shift towards renewable energy.

Speed up cash collection with FundNow

Learn how you can get paid upfront on your sales invoices.

Comparing the Best Embedded Lenders for Accounts Payable: C2FO, Resolve, Settle, and Lendica

Managing accounts payable (AP) financing effectively can significantly enhance a business’s cash flow and financial efficiency. This post compares four top embedded lenders that offer accounts payable financing or reverse factoring products: C2FO, Resolve, Settle, and Lendica, highlighting their key features and benefits.

Who are the Top Embedded Lenders for Accounts Payable?

1. C2FO

• Overview: C2FO offers flexible early payment options with low fees and seamless ERP integration. Their Name Your Rate® technology allows users to set discount rates, providing customizable solutions.

• Funding Speed: Payments can be received as soon as the next day.

• Advance Rates: Typically between 80-100%.

• Technology: Robust platform with features like Invoice Central for easy management. This enables businesses to accelerate payments and manage cash flow efficiently without changing existing invoicing processes .

2. Resolve

• Overview: Resolve focuses on net terms and cash advances, integrating with common ERP and accounting systems for automated invoice processing.

• Funding Speed: Often within days of invoice approval.

• Advance Rates: Up to 90%.

• Technology: Advanced integration and automation for seamless management. Resolve leverages the buyer’s creditworthiness to offer lower fees and ensures quick access to working capital, making it a reliable choice for improving cash flow .

3. Settle

• Overview: Designed for AP automation and working capital solutions, Settle offers strong integration with accounting software and ERP systems.

• Funding Speed: Typically within one business day.

• Advance Rates: Up to 100%.

• Technology: Comprehensive automation for invoice capture and approval. Settle’s platform helps businesses streamline their financial operations, saving time and reducing manual errors .

4. Lendica

• Overview: Lendica stands out with extensive connectivity, integrating with all public and private ERP and POS systems. Their AI-powered underwriting expands access to capital.

• Funding Speed: Instant funding decisions, typically within 24 to 48 hours.

• Advance Rates: Up to 100%.

• Technology: Advanced AI for smarter underwriting and streamlined processes. Lendica’s broad connectivity and rapid funding make it an exceptional choice for businesses seeking efficient and flexible AP financing solutions.

Comparing the Best Embedded Lenders for Accounts Payable

Category

C2FO

Resolve

Settle

Lendica

Fees

Typically low fees based on discount rates set by users. No upfront costs or hidden fees.

Fees vary; usually lower than traditional factoring, leveraging buyer’s credit rating.

Fees depend on services; competitive and transparent for AP automation and working capital solutions.

Rates start at 1% for 30 days.

Integration with ERP & POS Systems

Seamless integration with various ERP systems; no changes required to invoicing processes.

Integrates with common ERP and accounting systems, providing seamless invoice management.

Strong integration with accounting software and ERP systems to streamline AP processes.

Connects to all public and private ERP and POS systems, offering the widest connectivity in the market.

Loan Terms & Flexibility

Highly flexible; users can choose which invoices to accelerate and set discount rates.

Flexible terms based on buyer’s creditworthiness, ensuring favorable rates and terms.

Flexible working capital and AP solutions with customizable terms based on business needs.

Delay vendor payments up to 90 days with flexible payback schedules.

Funding Speed

Payments can be received as soon as the next day after terms are agreed upon.

Generally fast funding, often within days of invoice approval.

Rapid funding, often within one business day for qualified invoices.

Instant funding decisions, with quick access to funds, typically within 24 to 48 hours after approval.

Advance Rates

Typically between 80-100% depending on agreement with the buyer.

Up to 90% of the invoice value, depending on buyer’s credit rating and terms.

High advance rates, often up to 100%, subject to invoice and buyer terms.

Advance rates up to 100%, leveraging AI for smarter underwriting decisions.

Technology & Automation Features

Robust platform with features like Name Your Rate® and Invoice Central for easy invoice management and early payment requests.

Advanced technology for seamless integration and management of reverse factoring processes.

Comprehensive automation for AP processes, including invoice capture, approval rules, and integration with accounting systems.

Advanced AI-powered technology for underwriting and automated processes. Integrated with ERP and POS systems for streamlined loan and payment processes.

Eligibility Requirements

Accessible to small and mid-sized businesses; eligibility depends on buyer’s participation in C2FO program.

Based on buyer’s creditworthiness; favorable for suppliers with reliable buyers.

Suitable for startups and growing businesses; flexible criteria based on business needs and customer profiles.

Tailored to small and medium-sized businesses with specific requirements based on industry and business model. Expands reach beyond typical lenders using AI.

Why ERP Integration Matters as an Embedded Lender Paying Vendors

Enhance Efficiency

ERP integration ensures that all financial transactions and data are synchronized seamlessly. This automation reduces manual entry errors, saves time, and enhances overall efficiency in managing accounts payable. By integrating with ERP systems, embedded lenders like Settle and Lendica enable businesses to manage their invoices and payments within the same platform they use for other financial operations.

Improve Cash Flow Management

Real-time visibility into payable and receivable accounts is crucial for effective cash flow management. Embedded lenders that integrate with ERP systems provide businesses with up-to-date information on their financial status, helping them make informed decisions and maintain a healthy cash flow.

Simplify Operations

Integration with ERP systems streamlines financial operations, reducing administrative burdens and freeing up resources for other critical business activities. This simplification is particularly beneficial for small and medium-sized businesses that may lack the resources to manage complex financial processes manually.

For instance, Lendica’s ability to connect with all public and private ERP and POS systems ensures seamless transactions and data synchronization, making it easier for businesses to manage their AP processes effectively.

Simplify your process whenever you can.

How to Save Money with Embedded Lenders for A/P

Lower Fees

Choosing the right embedded lender can lead to significant cost savings through lower fees. Lenders like Resolve and Lendica offer competitive rates by leveraging the buyer’s credit rating, which can reduce the overall cost of financing. These lower fees make it more affordable for businesses to access the capital they need to maintain operations and growth.

Automation

Automation features provided by embedded lenders save time and reduce the need for manual intervention in AP processes. For example, Settle’s comprehensive automation capabilities help businesses capture invoices, manage approvals, and process payments more efficiently, reducing the time and labor costs associated with these tasks.

Instant Decisions

Lendica’s AI-powered platform provides instant funding decisions, reducing the wait time and administrative overhead associated with traditional financing methods. This rapid decision-making process allows businesses to access funds quickly, improving their cash flow and operational efficiency.

By utilizing these cost-saving features, businesses can manage their AP financing more effectively, reducing expenses and improving overall financial health.

Lendica’s AI-powered platform provides instant funding decisions… allowing businesses to access funds quickly, improving their cash flow and operational efficieny.

Lendica Lens underwriting guide

The Importance of Eligibility Requirements When Seeking an A/P Facility

Broader Access to Capital

Eligibility requirements play a crucial role in accessing AP financing. Lendica’s AI-driven underwriting expands access to capital by evaluating a broader range of data points, making financing available to more businesses, including those that might not qualify under traditional criteria. This inclusivity is particularly beneficial for small and medium-sized businesses seeking to improve their cash flow.

Flexible Criteria

Settle and Lendica offer flexible criteria tailored to business needs, ensuring that startups and growing businesses can access the funds they need. These lenders consider various factors beyond traditional credit scores, allowing more businesses to qualify for financing and maintain healthy cash flow.

By understanding and meeting these eligibility requirements, businesses can secure the AP financing they need to support growth and stability.

Conclusion: Lendica Outperforms Top Rated Embedded Lenders in Accounts Payable Financing

Lendica stands out among top embedded lenders for accounts payable financing due to its unique features:

• Extensive Connectivity: Integration with all public and private ERP and POS systems ensures seamless transaction handling and data synchronization.

• AI-Powered Decisions: Smarter underwriting decisions expand access to capital, making financing available to a broader range of businesses.

• Instant Funding: Quick access to funds with instant decisions and high advance rates up to 100%.

By leveraging advanced technology and providing broad connectivity, Lendica offers unparalleled benefits, making it the superior choice for businesses seeking efficient and flexible AP financing solutions.

In the evolving landscape of supply chain finance, reverse factoring is emerging as a transformative solution. Particularly within the wholesale business space, this financial tool is gaining traction for its ability to optimize cash flow, reduce credit risk, and strengthen supplier relationships. This article delves into the details of reverse factoring, its operational mechanics, and the compelling reasons behind its rapid adoption across many sector.

What is Reverse Factoring?

Reverse factoring, also known as supply chain financing, is a financial solution where a third-party financier, typically a bank or a specialized financial institution, facilitates early payment to suppliers on behalf of the buyer. Unlike traditional factoring where suppliers seek financing against their receivables, reverse factoring is initiated by the buyer to ensure their suppliers get paid faster. This shift in approach provides significant benefits to both parties involved in the transaction.

Delay supplier payments with Lendica

Learn how you can pay your suppliers early, enjoy early-pay discounts and pay back up to 90 days later.

1. Agreement Setup: The buyer begins by entering into an agreement with a financial institution to set up a reverse factoring program. This may be through an online application process, a bank due diligence questionnaire, or for certain embedded lenders, a one click approval.

2. Invoice Approval: The supplier delivers goods or services to the buyer and submits the corresponding invoice for approval. This may occur on a one-time or ongoing basis. It is important to work with your reverse factoring company to clarify which invoices will qualify for financing as certain invoices such as utilities, payroll, or other service-related expenses typically are unfundable.

3. Buyer Approval: The buyer verifies and approves the invoice, committing to pay the financial institution on the agreed-upon date. It is important to understand the fees your are paying at the time of approval.

Pricing: reverse factoring companies often charge a processing fee (usually 1% or less) and a factoring or financing fee.

4. Financier Payment: Upon approval, the financial institution pays the supplier the invoice amount, often at a discounted rate, before the invoice’s due date.

Note: make sure that your vendor is made aware that they will receive payment from a third party. In many cases, your reverse factoring provider will send automated emails with details of the invoice description. It is important to verify the financier payment process to ensure smooth supplier relationships.

5. Buyer Payment: The buyer then pays the financial institution the full invoice amount on the new due date. This may be the original due date or, in many cases, a delayed due date.

To illustrate how reverse factoring works, let’s consider a practical example involving a buyer named ChemShop Co., a vendor named Plastics Inc., and a financier named Lendica.

Invoice Issuance and Approval

• March 21st: Plastics Inc. delivers a shipment of raw materials to ChemShop Co. and issues an invoice for $10,000, due on March 31st.

• March 21st: ChemShop Co. approves the invoice and confirms the payment terms with Plastics Inc.

2. Initiation of Reverse Factoring

• March 22nd: ChemShop Co. initiates a reverse factoring arrangement with Lendica, a financial institution specializing in supply chain financing. ChemShop agrees to terms provided by Lendica, 1% processing fee a 1.5% financing fee with payment made on April 30th.

3. Payment to Supplier

• March 31st: Lendica, acting on behalf of ChemShop Co., pays Plastics Inc. the full invoice amount of $10,000. This ensures that Plastics Inc. receives the payment on the due date without delay.

4. Fee Charged to Buyer

• April 1st: Lendica charges ChemShop Co. a fee for the reverse factoring service. In this case, the fee is $100, or 1% of the invoice amount.

5. Repayment by Buyer

• April 30th: ChemShop Co. repays Lendica the total amount of $10,150. This includes the original invoice amount of $10,000 plus an additional fee of $150 (1.5% of the invoice amount for the 30-day period).

Why Reverse Factoring Works for Wholesalers

Wholesalers, especially those operating in a sector marked by complex supply chains and stringent payment terms, can reap substantial benefits from reverse factoring. Here’s how:

1. Improved Cash Flow: Reverse factoring ensures that suppliers receive payments promptly, significantly improving their cash flow. This is particularly beneficial in industries where large working capital outlays are common.

2. Reduced Credit Risk: By leveraging the buyer’s creditworthiness, suppliers can access financing at more favorable terms, reducing their credit risk.

3. Stronger Supplier Relationships: Prompt payments foster better relationships with suppliers, ensuring a more reliable and collaborative supply chain.

Build strong vendor relationships by consistently paying your bills early or on time.

4. Cost Savings: Suppliers often offer discounts for early payments. By using reverse factoring, buyers can capitalize on these discounts, leading to cost savings.

5. Enhanced Operational Efficiency: The automated nature of reverse factoring streamlines the payment process, reducing administrative burdens and operational inefficiencies.

Reverse Factoring: The Fastest Growing Form of Factoring

Recent studies, including those by McKinsey & Company, highlight the exponential growth of reverse factoring as a preferred financing tool. McKinsey reports that the global market for reverse factoring is expanding rapidly, driven by its proven benefits in enhancing liquidity and optimizing working capital management.

Evidence from McKinsey & Company

McKinsey’s analysis underscores several factors contributing to the swift adoption of reverse factoring:

• Technological Advancements: Innovations in financial technology have made reverse factoring more accessible and efficient.

• Market Demand: The increasing need for liquidity and financial stability in volatile markets has propelled the demand for reverse factoring.

• Regulatory Support: Favorable regulatory frameworks in various regions have facilitated the growth of reverse factoring programs.

Conclusion: Why Reverse Factoring is Ideal for Wholesalers

Wholesaler businesses, characterized by their capital-intensive nature and complex supply chains, stands to gain immensely from reverse factoring. Here’s why:

1. Capital Intensity: Wholesalers often deal with substantial working capital expenditures. Reverse factoring provides a reliable source of liquidity, enabling them to manage these costs more effectively.

2. Supply Chain Complexity: With numerous suppliers and extended payment terms, reverse factoring helps wholesalers maintain a smooth flow of operations by ensuring timely payments.

3. Market Volatility: Many industries are subject to price fluctuations and demand variability. Reverse factoring offers financial stability, allowing distributors to navigate market volatility with greater confidence.

4. Global Trade: As many wholesalers operate globally, reverse factoring facilitates smoother international transactions by mitigating currency and credit risks.

5. Sustainability Goals: By ensuring suppliers are paid promptly, reverse factoring contributes to more sustainable and resilient supply chains, aligning with the broader sustainability goals of many companies.

Conclusion

Reverse factoring is revolutionizing the way wholesalers manage their finances and supply chains. By offering improved cash flow, reduced credit risk, and stronger supplier relationships, it stands out as a powerful tool for the industry. Backed by technological advancements and growing market demand, reverse factoring is poised to become an integral part of financial strategies in many sectors. As McKinsey & Company’s research indicates, the rapid adoption of this financing solution is not just a trend but a significant shift towards more efficient and resilient supply chain management. For wholesalers looking to stay competitive and financially robust, embracing reverse factoring is a strategic move towards a more sustainable and prosperous future.

Delay supplier payments with Lendica

Learn how you can pay your suppliers early, enjoy early-pay discounts and pay back up to 90 days later.

Who are the top embedded lenders for accounts receivable

In the competitive landscape of wholesale, managing cash flow efficiently is essential for success. One increasingly popular solution is accounts receivable (A/R) financing through embedded lenders. These lenders purchase your outstanding invoices, converting them into immediate cash. However, the real advantage comes when these lenders are integrated into your existing ERP (Enterprise Resource Planning) systems. This article will compare top embedded lenders that purchase A/R, focusing on why Lendica stands out as the optimal provider for small and medium-sized wholesalers.

AI-driven underwriting to deliver widest approval and lowest rates

Based on customer creditworthiness, flexible for various industries

No minimum credit score, $15,000 monthly revenue recommended

Low credit score accepted, minimal paperwork, no financials up to $350k

Why ERP integration matters as an embedded lender purchasing receivables

Streamlined operations

ERP systems consolidate various business functions, providing a unified platform for managing inventory, orders, and financials. When an embedded lender like Lendica integrates with your ERP, it automates the A/R financing process, reducing manual data entry and errors. This seamless integration saves significant time and ensures that all departments have real-time access to critical financial information.

Real-time financial insights

With ERP integration, businesses gain instant visibility into their financial health. Lendica’s integration allows you to quickly identify eligible invoices for financing, making informed decisions about cash flow management. This real-time insight is crucial for maintaining operational efficiency and ensuring timely payments to suppliers.

How to save money with embedded lenders

Lower financing costs

Choosing a lender with competitive rates is vital for minimizing financing costs. Lendica offers one of the best rates in the market, starting at 1% for 30 days. This affordability, combined with seamless ERP integration, allows businesses to maximize their savings. Lower financing costs mean more funds available for other critical business activities. You may also consider 1st Commercial Credit with rates starting at 0.69% per month.

Reduced administrative overhead

By automating invoice submissions and payments through ERP integration, Lendica significantly reduces administrative overhead. This automation eliminates the need for manual data handling, freeing up resources for more strategic tasks. The savings in time and labor can be substantial, translating into direct financial benefits for your business.

Avoid manual processes to save you time and money in the long run.

Enhanced cash flow management

Effective cash flow management is essential for growth. Embedded lenders like Lendica provide real-time updates through ERP integration, helping businesses maintain a healthy cash flow. Knowing exactly when funds will be available allows for better financial planning and reduces the need for costly short-term borrowing.

Time and cost savings from automation

By integrating with your ERP, Lendica automates both the invoicing and accounting processes. This automation can save your business up to 200 hours per year, translating into approximately $20,000 in cost savings. These savings highlight the efficiency and cost-effectiveness of using an embedded lender integrated into your ERP system.

This automation can save your business up to 200 hours per year, translating into approximately $20,000 in cost savings.

Lendica research team

The importance of eligibility requirements when seeking an A/R facility

Data-driven AI lender

Lendica stands out due to its data-driven, AI-powered approach to lending. Traditional lenders often rely on rigid criteria that may not accurately reflect a business’s potential. In contrast, Lendica’s AI system continuously learns from your business data, getting more comfortable with risks that other lenders might overlook. This deeper understanding allows Lendica to offer more tailored financing solutions, ensuring that you get the best possible terms.

Speed of approvals

In the fast-paced world of wholesale, speed matters. Lendica offers some of the fastest approval times in the industry, often providing funding within 24 to 48 hours. Quick access to funds ensures that your business can seize new opportunities, manage unexpected expenses, and maintain smooth operations without disruptions.

Conclusion: Lendica outperforms top rated embedded lenders in accounts receivable financing

ERP integration is crucial for businesses seeking to optimize their accounts receivable financing. Among the embedded lenders compared, Lendica stands out due to its competitive rates, seamless integration, and AI-driven approach. By choosing Lendica, businesses can save significant time and money, reduce administrative overhead, and maintain a healthy cash flow.

Investing in an embedded lender like Lendica not only enhances your financial management but also positions your business for long-term success. For small and medium-sized wholesalers, these benefits are critical for maintaining competitiveness and achieving sustainable growth. Consider Lendica to leverage these advantages and drive your business forward.

Managing accounts receivable (A/R) can be a complex and risky task for many businesses. Selling A/R to an embedded lender offers a streamlined solution that can mitigate credit risk, enhance cash flow, and automate accounting processes. In this guide, we’ll walk you through the steps to successfully sell your A/R to an embedded lender and highlight the key benefits of this approach.

Step 1: Understand Your A/R Portfolio

Before selling your A/R, it’s crucial to assess your portfolio. Identify which accounts receivable you want to sell, focusing on those with higher credit risk or longer payment terms. Understanding your A/R portfolio helps you determine which receivables are best suited for sale and maximizes the benefits you can gain from this process.

Remember: You don’t always have to sell your entire portfolio to the lender. In some cases, you may be able to sell only part of your accounts receivable and still maintain certain customer segments.

Step 2: Choose the Right Embedded Lender

Selecting the right embedded lender is vital. Look for a lender that integrates seamlessly with your ERP system to ensure smooth operations. Evaluate potential lenders based on their terms, fees, and support services. A good embedded lender should offer transparent terms and robust customer support to guide you through the process.

Important: Make sure the embedded lender can integrate directly with your ERP. If they cannot, you may be at risk of significant ongoing maintenance which will reduce any benefits from the sale.

Step 3: Integrate the Embedded Lender with Your ERP

Preparation is crucial for a successful A/R sale. Gather necessary documentation, including invoices, payment histories, and customer information. Ensure your A/R is well-organized and presented attractively to potential lenders. This preparation can make your receivables more appealing and streamline the sale process.

Bonus: If you are already using an ERP that works with the embedded lender, this process may be automated. For customers that use Datacor, for example, their preferred embedded lending is integrated directly into certain A/R and A/P tables.

Step 5: Negotiate Terms with the Lender

Negotiating favorable terms with your lender is essential. Key points to discuss include:

• Advance rates: The percentage of the receivable’s value the lender will advance.

• Fees: Understand all fees involved to avoid hidden costs.

• Recourse terms: Determine if the lender requires you to buy back uncollected receivables.

Securing favorable terms maximizes the financial benefits and ensures a smooth transaction.

When negotiating, remember that the lender may not have the full picture of your business. You may have an advantage of working with certain customers for long periods of time and, in doing so, have established trusting relationships that the lender may not price in. If the lender gives you a bad rate, chances are they aren’t adept at risk-based pricing.

Tip: Ask the lender how they do their underwriting. If they are not using historical customer ordering patterns or advanced data modeling on top of your ERP history, chances are they will not be accurately pricing your receivables.

Speed up cash collection with FundNow

Learn how you can get paid upfront on your sales invoices.

Before proceeding, make sure to dig into any hidden fees lying below the surface of an otherwise good deal.

Step 6: Execute the Sale

Once terms are agreed upon, execute the sale. This typically involves:

• Signing a contract with the lender.

• Transferring the agreed-upon receivables to the lender.

• Receiving the advance payment from the lender.

Ensure you comply with any legal or regulatory requirements during this process.

Look out for “delayed purchase prices” that will involve the lender paying you out, be it partially or totally, upon collection of the receivables. Lenders may promise a small percentage of the receivables upfront and remit the remainder upon collection from your customers. This can be customary, but make sure you review the agreement with your legal and financial advisors prior to agreeing to avoid any unsavory clauses.

Step 7: Manage Post-Sale Operations

After selling your A/R, manage post-sale operations efficiently. Maintain communication with your customers to ensure they are aware of the new payment arrangements. The lender will typically handle collections, but it’s important to stay involved to address any issues that may arise and ensure customer satisfaction.

In some cases, the lender will remain behind the scenes while in others the lender will take over the credit process on your behalf. It is important to weigh the pros and cons of bringing a third party into a customer transaction but, if you are able to find the right embedded lender, it can be a huge benefit.

Benefits of Selling A/R to an Embedded Lender

1. Remove Credit Risk

By selling your A/R, you transfer the risk of non-payment to the lender. This allows you to focus on business growth without worrying about delinquent accounts. According to a recent Atradius Study, more than 55% of invoices in 2023 were not paid on time, and with each delayed invoice comes added operational drag.

More than 55% of invoices in 2023 were not paid on time

Atradius B2B Payment Trends for 2023

2. Boost Cash Flow

Selling A/R provides an immediate cash infusion, enhancing your liquidity. Use this increased cash flow to invest in inventory, operations, or expansion.

3. Automate Accounting

Integration with your ERP system automates the accounting process. This reduces manual work, minimizes errors, and keeps your financial records up-to-date.

4. Control Customer Interaction

Maintain control over how and when customers are involved in the process. By involving customers on your terms, you enhance their experience and ensure they are informed and engaged.

Conclusion

Selling A/R to an embedded lender offers numerous advantages, including reduced credit risk, improved cash flow, automated accounting, and controlled customer interactions. By following this guide, you can streamline the process and unlock the financial and operational benefits of selling your A/R. Consider this option to enhance your business’s financial stability and efficiency.

Speed up cash collection with FundNow

Learn how you can get paid upfront on your sales invoices.

BOSTON, April 16, 2024 /PRNewswire/ — Lendica, an embedded AI lending, and EBizCharge, a top-rated provider of payment solutions, proudly announce a transformative collaboration aimed at introducing a groundbreaking embedded business credit solution for small and medium-sized enterprises in the U.S.

The new service, called the iBranch, is a cutting-edge financing solution that enables businesses to borrow money from Lendica without having to switch to a different platform. The innovative service represents a fusion of Lendica’s cutting-edge AI credit underwriting and EBizCharge’s all-in-one suite of payment solutions. This synergy facilitates a seamless and efficient financing process, allowing businesses to access fast and low-cost funding without the need to transition to a different platform.

As an industry leader, EBizCharge aims to seamlessly connect payments through its dynamic and comprehensive software. By integrating payments and financing through this new partnership, companies are empowered to grow and scale faster. This all-inclusive approach streamlines operations and enhances overall efficiency for businesses.

Leveraging the growing trend of embedded lending popularized by industry giants like Amazon, Shopify, and Square, the iBranch is set to become a key player in meeting the credit needs of small and mid-sized businesses. Embedded business loan origination is projected to experience a staggering 125% year-over-year growth, reaching an annual origination of $500 billion by 2030.

“We’re excited to partner with EBizCharge, an industry leader in payment solutions software. This is a mutually beneficial partnership, as we can use our AI credit underwriting to offer fast and low-cost financing solutions for businesses,” Jared Shulman, CEO and co-founder of Lendica, expresses his enthusiasm about the partnership. “Traditional small business credit is very expensive, with the average borrower paying 61% APR. Our embedded lending programs can dramatically lower rates to our customers we’re excited to bring them to market with a leader in the space.”

Jerry Shu, the company’s CTO/Co-founder, adds that the power of AI-driven credit underwriting shines with rich, embedded datasets that banks and non-bank lenders struggle to process. This is especially useful for instant decision transactions such as B2B Buy Now Pay Later (BNPL) and other shorter term cash management tools.

“EBizCharge is the ultimate platform for payment solutions. With the iBranch, we’re adding financial power to our platform, allowing our customers to access credit without leaving the EBizCharge platform,” said Matt Rogers, VP of Strategic Alliances at EBizCharge.

Lendica enhances the financing experience for businesses, offering features such as instant decisions, fair pricing with low rates and fees, and no credit impact, providing flexibility even in cases of rejection. This strategic alliance is expected to significantly impact the payments sector by offering customers unique access to fast, affordable capital sources that support growth and can help businesses scale directly from the EBizCharge platform.

To learn more about Lendica and its transformative potential for your business, please visit www.golendica.com. Stay connected and follow us on LinkedIn.

BOSTON, Jan. 30, 2024 /PRNewswire/ — Lendica, an embedded AI lending company, and CSG Forte, a CSG® (NASDAQ: CSGS) company and a leader in complete and customizable digital payments, announce a strategic partnership to deliver an embedded business credit solution to small and medium sized US companies.

Lendica and CSG Forte’s offering, called the iBranch, is an embedded financing service that enables SMBs to borrow money from their software vendors instead of traditional financial institutions.

Embedded lending, popularized by software companies such as Amazon, Shopify, and Square, has become a growing source of credit made available to small businesses. It is estimated that embedded business loan origination is growing at roughly 125% year over year and will hit an annual $500bn origination by 2030.

CSG Forte is partnering with Lendica, a leader in embedded lending solutions, to bring the solution to its Independent Software Vendor (ISV) partners and their merchants.

“Traditional small business credit is very expensive with the average borrower paying 61% APR.” shares Jared Shulman, CFA, Lendica’s CEO/Co-founder. “Our embedded lending programs, when implemented effectively, dramatically lowers rates to our customers by leveraging private datasets for more effective underwriting and better sales channels to cut customer acquisition costs.”

Jerry Shu, the company’s CTO/Co-founder, adds that the power of AI-driven credit underwriting shines with rich, embedded datasets that banks and non-bank lenders struggle to process.

The benefits of embedding lending extend beyond happier and healthier borrowers. ISVs benefit as well, earning a portion of the fee revenue generated from their embedded lending program and experience enhanced customer loyalty.

Through this partnership, CSG Forte’s diverse range of ISV partners and their merchants, including those in industries like field services and property management, can benefit from an innovative, embedded lending experience. For example, property management merchants may leverage this easy-to-use solution to access capital for building repairs and needed supplies or to engage in professional services to promote their business. The easy access to affordable capital empowers merchants and elevates their potential for future growth.