Introduction

Welcome to the Lendica Glossary. This comprehensive guide helps to explain key financial terms and concepts relevant to embedded lending and business financing. Whether you’re a small business owner, CFO, or financial enthusiast, this glossary will help you understand essential terms and how they apply to your financial operations.

Terms

2/10 Net 30

A payment term offering a 2% discount if an invoice is paid within 10 days; otherwise, the full amount is due in 30 days. This incentivizes early payment and improves cash flow.

Example Formula:

Discount Amount = Invoice Amount × 0.02

Use 2/10 Net 30 for free finance

Learn a reverse factoring hack for scaling.

Accounts Payable

Money owed by a business to its suppliers for goods or services received but not yet paid for. Managing A/P effectively is crucial for maintaining good supplier relationships and ensuring the business has adequate cash flow and operational liquidity.

Accounts Receivable

Money owed to a business by its customers for goods or services provided but not yet paid for. Managing A/R effectively is crucial for maintaining cash flow and operational liquidity.

Days Inventory Outstanding (DIO)

Measures the average number of days inventory is held before it is sold.

Example Formula:

If a company has an average inventory of $50,000 and a COGS of $200,000, the DIO would be 50,000/200,000 x 365 = 91.25 days.

Days Payables Outstanding (DPO)

Measures the average number of days a company takes to pay its suppliers.

Example Formula:

If a company has accounts payable of $30,000 and a COGS of $200,000, the DPO would be 30,000/200,000 x 365 = 54.75 days.

Days Sales Outstanding (DSO)

Measures the average number of days it takes to collect payment after a sale.

Example Formula:

If a company has accounts receivable of $25,000 and total credit sales of $150,000, the DSO would be 25,000/150,000 x 365 = 60.83 days.

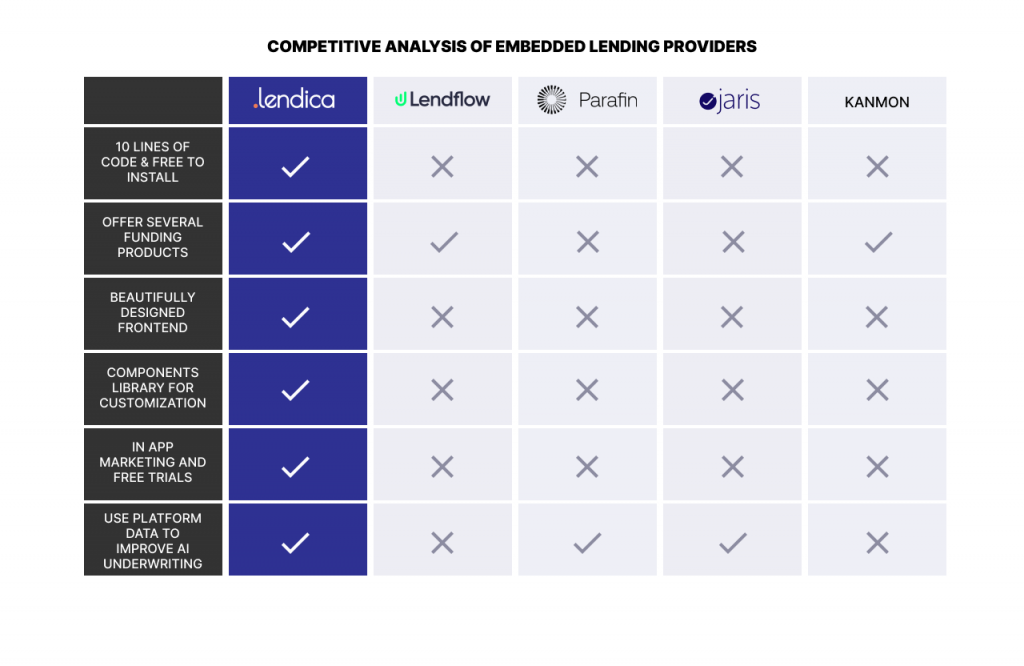

Embedded Lending

A financial service integrated within a software platform, enabling users to access credit seamlessly. It simplifies the borrowing process and enhances user experience by providing financial services within existing workflows.

Enterprise Value

Enterprise Value (EV) is a measure of a company’s total value, often used as a more comprehensive alternative to market capitalization. It includes the market cap, debt, minority interest, and preferred shares, minus total cash and cash equivalents. EV is useful in assessing the value of a business for potential acquisition.

Example Formula:

Enterprise Value = Market Capitalization + Total Debt + Preferred Shares + Minority Interest – Cash and Cash Equivalents

For instance, if a company has a market cap of $50 million, total debt of $10 million, and $5 million in cash, its EV would be $55 million.

ERP Integration

The process of connecting a company’s Enterprise Resource Planning (ERP) system with other applications to streamline operations and ensure consistent data flow. It improves efficiency and accuracy in financial management.

Factoring

A financial transaction where a business sells its accounts receivable to a third party at a discount to receive immediate cash. This helps businesses manage cash flow and reduce credit risk.

Speed up cash collection with FundNow

Learn how you can get paid upfront on your sales invoices.

Factor Rate

A factor rate is a fixed multiplier used to determine the total repayment amount in a merchant cash advance or factoring agreement. Unlike traditional interest rates, factor rates are expressed as a decimal figure, typically ranging from 1.1 to 1.5. The total repayment amount is calculated by multiplying the advance amount by the factor rate.

Example Formula:

Total Repayment Amount = Advance Amount × Factor Rate

For instance, if the advance amount is $10,000 and the factor rate is 1.2, the total repayment would be $12,000.

Reverse Factoring

A financial arrangement where a third party finances a company’s suppliers, allowing the suppliers to get paid early while the company pays the third party later. It enhances supplier relationships and improves cash flow management.

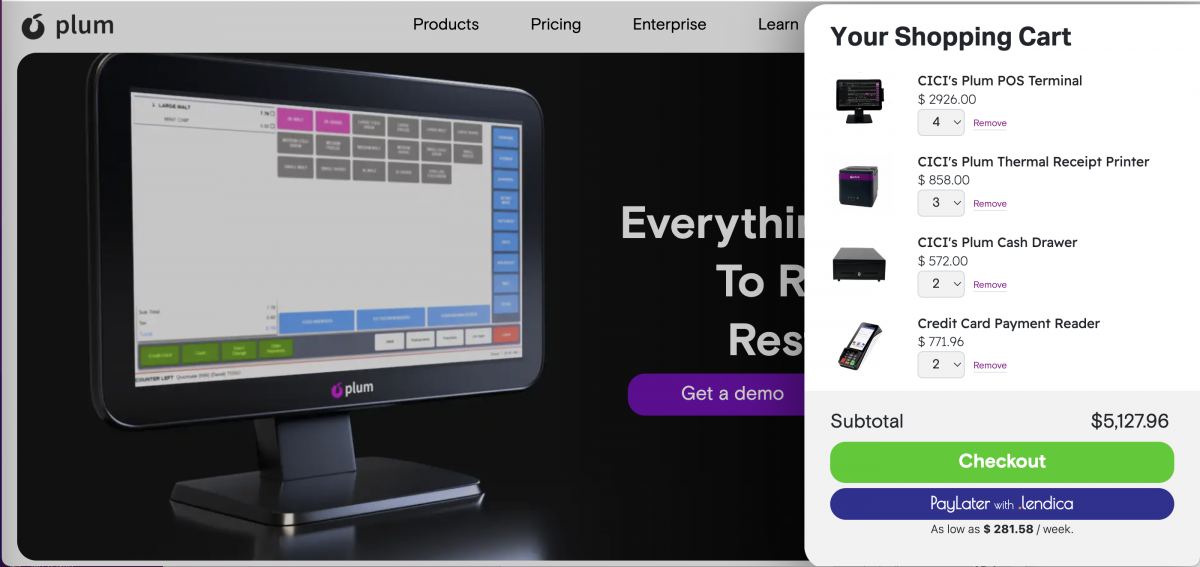

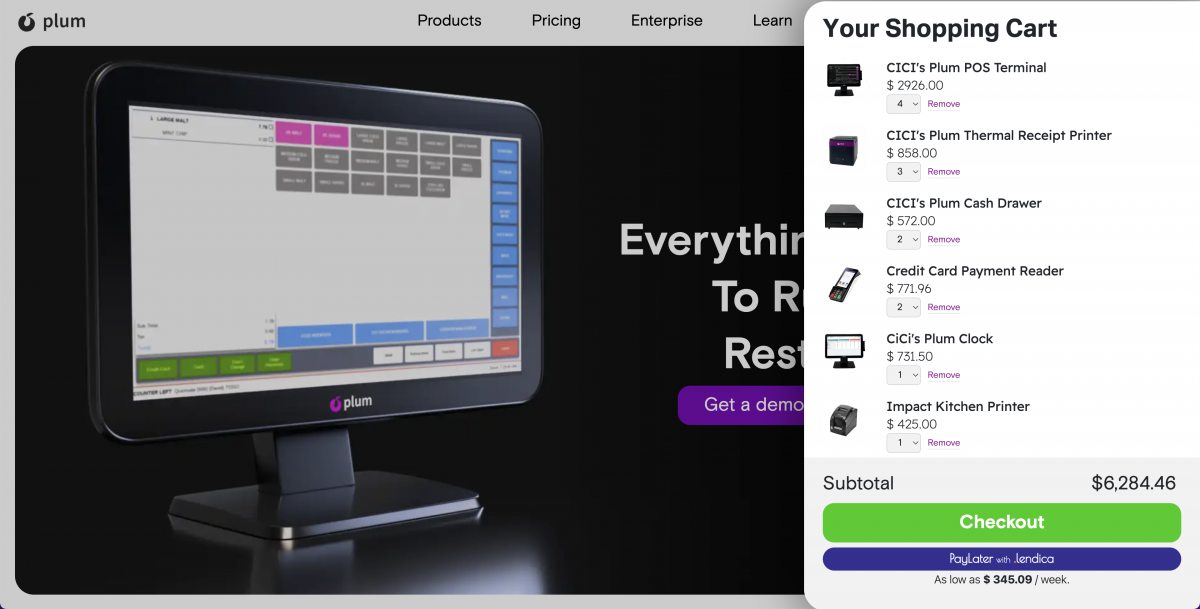

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.

Use 2/10 Net 30 for free finance

Learn a reverse factoring hack for scaling.

Small Bill Charges

Additional fees that a service provider applies for processing smaller invoices or bills, typically to cover administrative or processing costs. These charges are often implemented to ensure that even smaller transactions remain cost-effective for the business providing the service.

Vertical SaaS

Vertical SaaS is software designed specifically for the needs of a particular industry or niche, such as healthcare or finance. It provides specialized features and solutions tailored to the unique challenges of that sector.

Working Capital

The difference between a company’s current assets and current liabilities, representing the liquidity available for day-to-day operations. Effective management of working capital is essential for maintaining business solvency.

Example Formula:

Working Capital = Current Assets – Current Liabilities

Speed up cash collection with FundNow

Learn how you can get paid upfront on your sales invoices.

Delay vendor payments with PayLater

Learn how you can pay your vendors early, enjoy early-pay discounts and pay back up to 90 days later.